Welcome again to our sequence on leverage bank card multipliers to maximise your incomes potential. In Half 1, we targeted on playing cards issued by American Specific.

American Specific is a good financial institution to build up factors with due to its huge array of switch companions obtainable via American Specific Membership Rewards. It additionally has co-branded playing cards with Air Canada, making it simple to build up Aeroplan factors, a significant participant in our Canadian panorama.

Sadly, not all retailers settle for Amex, on condition that it tends to levy increased service provider processing charges. Undoubtedly there’ll be instances you’ll have to tug out a Mastercard or Visa, so in Half 2 of this sequence, we’ll now have a look at class incomes multipliers on playing cards issued by different banks.

For simplicity’s sake, we’ll solely give attention to Canadian playing cards that earn airline factors currencies or their equal, versus money again playing cards or different fixed-value factors currencies.

Canadian Banks with Airline Companions

American Specific has probably the most flexibility in relation to switch companions, with a complete of six airline companions and two lodge companions. Nevertheless, there are nonetheless some good Visa and Mastercard choices.

In Canada, RBC, CIBC, TD, Brim Monetary, and Neo Monetary all have bank cards with which you’ll be able to earn airline factors.

RBC

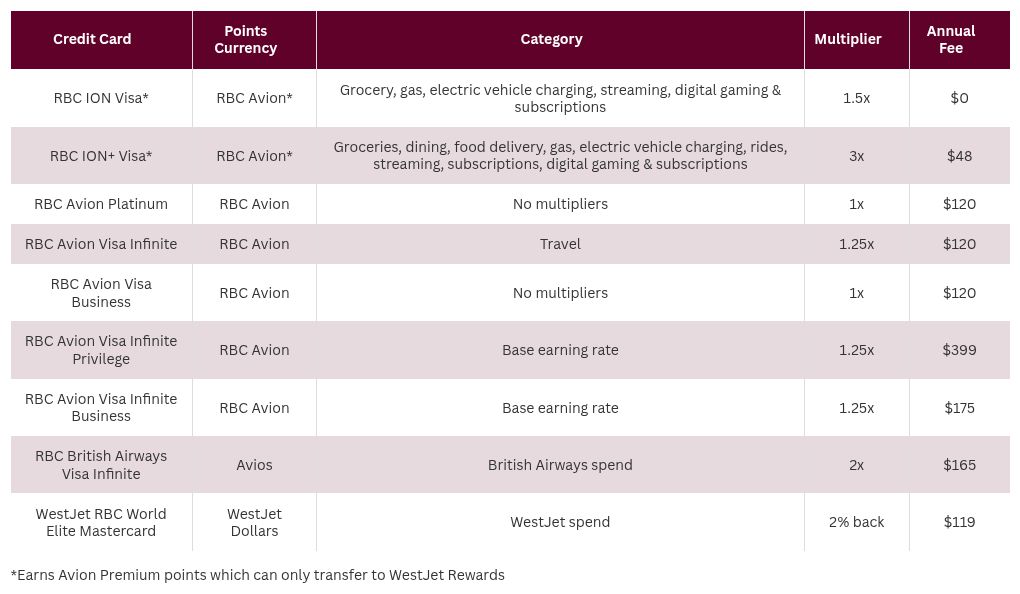

RBC provides a few bank cards that may earn airline currencies instantly:

RBC additionally has its personal line of Avion bank cards that earn RBC Avion factors. There are two tier of Avion factors: Avion Premium factors and Avion Elite factors.

The ION household of playing cards earns Avion Premium factors that are extra restrictive and may solely be transferred on to WestJet Rewards. All different Avion-branded playing cards earn Avion Elite factors, which will be transferred to 4 airline companions.

The switch ratios from RBC Avion to the airline currencies are as follows:

Protecting these companions and ratios in thoughts, let’s have a look at what the bank card multipliers are, if any:

The ION household of playing cards takes the prize for greatest earn charges, however for higher flexibility in reward redemption, you’ll need a card that earns Avion Elite factors just like the RBC Avion Visa Infinite card.

For the next base incomes charge of 1.25 factors per greenback spent, seize a premium card, however ensure you’ll be able to justify the upper annual charge (maybe by redeeming for enterprise class flights at 2 cents per level).

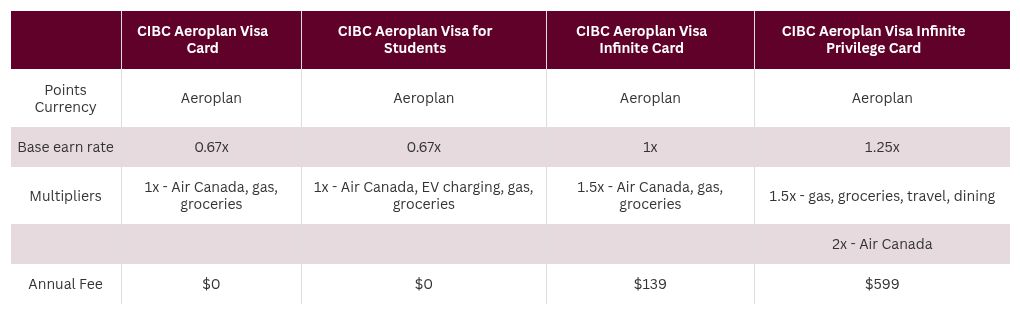

TD and CIBC

I’ve grouped TD and CIBC collectively as a result of they each solely have one airline program accomplice, Aeroplan, though take into account that any Aeroplan factors earned will be redeemed on any certainly one of Aeroplan’s many airline companions.

Each banks provide a number of completely different tiered Visa playing cards that may earn Aeroplan factors instantly:

Now let’s check out how their incomes charges examine:

Notice that for the TD playing cards with a Starbucks multiplier, you will need to hyperlink your TD bank card to your Starbucks account to earn the multiplier.

The earn charges between completely different tiers of TD and CIBC playing cards are moderately comparable, so when deciding between a TD or CIBC card, it could come right down to different elements corresponding to welcome bonuses and different bank card advantages.

For those who’re in search of a no-fee entry-level keeper card, then the CIBC Aeroplan Visa Card is an effective choice in comparison with the TD Aeroplan Visa Platinum Card, which expenses an $89 annual charge.

Take into account that TD and CIBC typically provide a primary 12 months free profit on their Visa Infinite playing cards, so with the upper earn charge, you might be higher off selecting certainly one of these playing cards for not less than the primary 12 months.

Brim Monetary

In 2022, Brim Monetary launched Canada’s first and solely Air France-KLM Flying Blue co-branded bank card, the Air France-KLM World Elite Mastercard.

The cardboard has the next earn charges:

- 1 Flying Blue mile per greenback base earn charge

- 2 Flying Blue miles per greenback spent on eating places and bars

Whenever you examine incomes strategies for Flying Blue miles, the Air France-KLM World Elite Mastercard can come out forward of transferring from American Specific. Whereas Amex permits you to convert Membership Rewards factors to Flying Blue miles at a 1:0.7 ratio, the direct incomes from the Air France-KLM card can show extra advantageous even with its modest incomes charges. The annual charge of $132 can also be on par with different mid-tier playing cards.

Periodically, Brim provides boosted earn charges when purchasing with choose accomplice retailers.

Neo Monetary

After RBC discontinued its Cathay Pacific Visa Platinum card and the HSBC World Elite Mastercard was phased out following RBC’s acquisition of HSBC in 2023, Neo Monetary stepped in to fill the hole. Although not extensively identified amongst Canadians, Neo Monetary now provides Canada’s sole Asia Miles co-branded bank card, the Cathay World Elite® Mastercard.

The cardboard takes a simple strategy to rewards; as an alternative of providing varied class multipliers, it differentiates between purchases made in Canadian {dollars} and people made in foreign exchange, encouraging its use when overseas.

The cardboard has the next earn charges:

- 1 Asia Mile per greenback spent on purchases made in Canadian {dollars}

- 2 Asia Miles per greenback spent on purchases made in foreign exchange

- 2 Asia Miles per greenback spent on Cathay Pacific flights

Although the earn charge is fairly normal for purchases made in Canadian {dollars}, the elevated earn charge on purchases made overseas helps offset the overseas transaction charge. You’ll additionally need to issue within the $180 annual charge which is on the upper finish.

Like Brim, Neo additionally provides elevated incomes charges with its retail companions.

Which Non-Amex Credit score Card Ought to You Use?

To find out which card will greatest maximize your earn, you’ll need to do a private evaluation to see what your spending and journey patterns are.

Your spending patterns will decide which multipliers pertain probably the most to you. Your journey patterns will decide which airline program you’ll need to put money into, what number of factors you might want, and whether or not you’ll be able to justify the upper annual charge of a card in trade for the opposite advantages which will include it.

If gathering Aeroplan factors is your purpose, the one non-Amex choices are a TD or CIBC Aeroplan Visa card. Which tier of card you select will rely upon what you spend probably the most on, whether or not your spend can justify the annual charge, and the welcome bonus on the time.

For those who can justify the annual charge of an Infinite Privilege card, you’ll maximize your earn with 1.25x as a base incomes charge and 1.5x on most main classes of spending.

For those who’re planning to fly on an airline that’s a part of the Oneworld alliance, then take into account your spending patterns.

For normal spending, it’s an in depth race between the RBC® Avion Visa Infinite Privilege card or RBC Avion Visa Enterprise card, which earn 1.25 Avios or Asia Miles per greenback spent. The Cathay World Elite® Mastercard is one other strong contender, because it earns a minimal of 1 Asia Mile per greenback spent, and is without doubt one of the few playing cards that supply a multiplier on spend in foreign exchange.

For those who discover worth within the American Airways AAdvantage program (ie. reserving Qatar Airways’ Qsuites with the bottom taxes and costs), then RBC Avion-earning playing cards could be the popular selection.

For households who journey to Europe recurrently, then Air France-KLM Flying Blue’s 25% off low cost on award tickets for kids will seemingly enchantment to you, and you might discover higher worth utilizing the Air France-KLM World Elite Mastercard in your each day spend.

For those who’re taking a look at the next base incomes charge, then you definately’ll need to have a look at the Visa Infinite Privilege playing cards, which all earn 1.25 factors per greenback spent as a base incomes charge, and 1.5 factors per greenback spent on eating.

The upper incomes charges alone, nonetheless, could not justify the excessive annual charge of $599, until you’ll be able to reap the benefits of the opposite advantages that include the cardboard.

For those who’re a Starbucks fan, then you definately’ll in all probability need to look right into a TD card moderately than CIBC, as they provide a 50% bonus when you hyperlink any TD Aeroplan card to your Starbucks account.

And eventually, holding each a Visa and a Mastercard in your pockets can also be an excellent technique as not all retailers will settle for each.

Conclusion

Sadly, there are nonetheless many retailers that don’t take American Specific, however that doesn’t imply it’s a must to cease incomes airline factors.

RBC, TD, CIBC, Brim Monetary, and Neo Monetary are all banks that supply Credit cards and Visas that may, in some instances, provide higher incomes charges on airline currencies than American Specific.

Take a while to research your personal spend and journey patterns and see which card or playing cards will allow you to obtain your journey targets sooner.

")